A few years back, a friend of mine was drowning in about $28,000 of credit card debt spread across six different cards. She was making minimum payments every month, watching the balances barely move, and quietly panicking. That’s when she started looking into debt settlement companies , and Freedom Financial Network kept showing up in her research. She asked me what I thought. I told her I’d dig into it properly before giving her an answer.

Debt relief companies are a mixed space. Some are legitimate, while others are scams. It can be hard to tell the difference, especially when you are under financial stress. The last thing you want is to join a service that makes your situation worse. You need to be careful before signing up for anything.

In this review, I will explain how Freedom Financial Network works. I will also cover the real costs. You will see who it is a good fit for. Just as importantly, you will learn who should look for other options. There are no affiliate deals or paid placements here. This is an honest breakdown.

What Is Freedom Financial Network and How Does It Work?

Low investment business ideas often attract people who want to improve their money situation. This company is based in San Mateo, California. It started in 2002. It runs several brands. Its main service is debt settlement. It has helped hundreds of thousands of people. It has also settled billions of dollars in debt. This makes it one of the largest companies in the United States.

Think of it like this: your creditors would rather get 50% of something than 0% of nothing if you went bankrupt. That’s the leverage FFN uses. The process typically takes 24–48 months, and it requires you to have at least $7,500 in unsecured debt , think credit cards, personal loans, medical bills , to qualify. It is not for secured debts like mortgages or car loans.

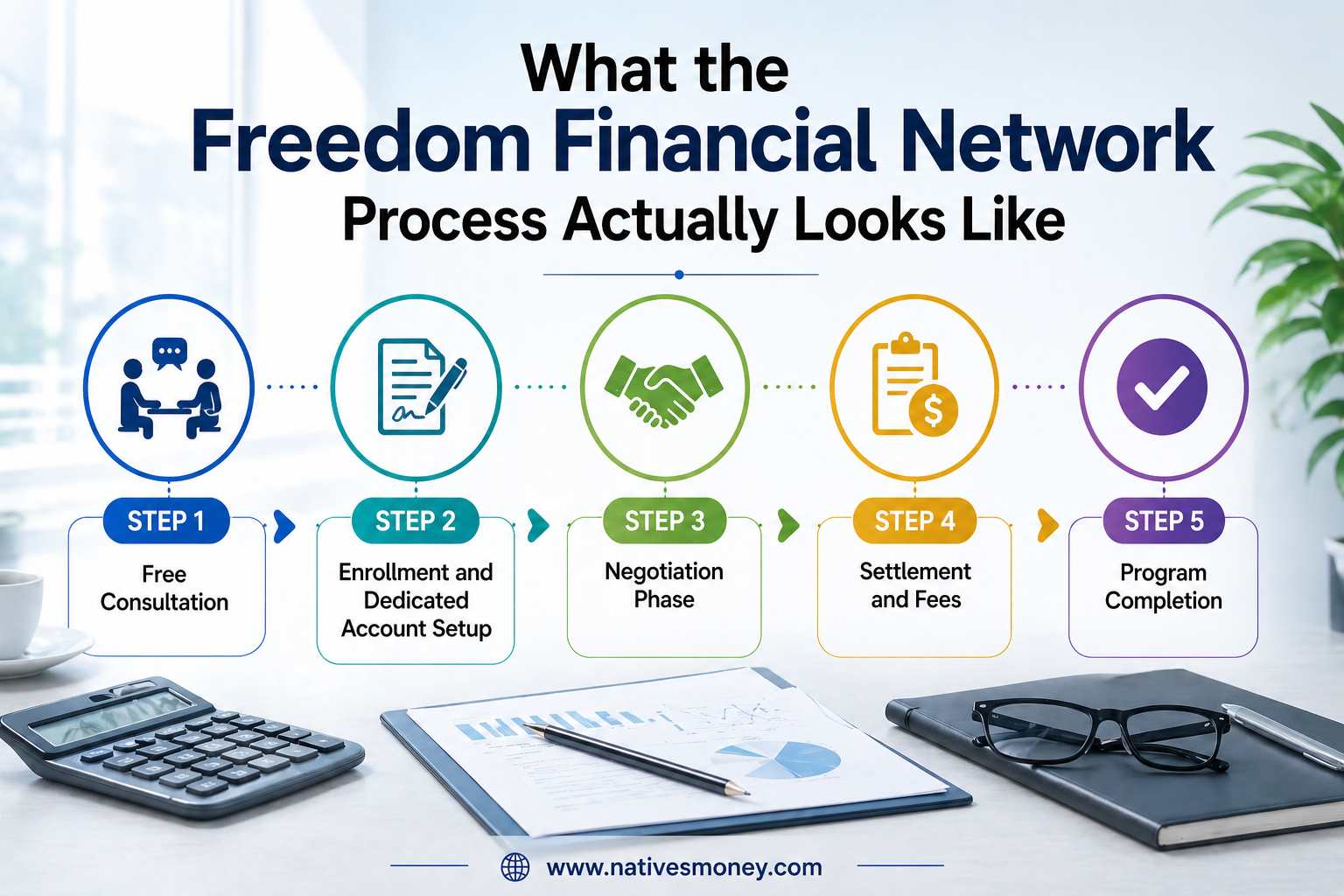

What the Freedom Financial Network Process Actually Looks Like

Understanding the step-by-step process before you enroll is critical. Here’s what happens from day one:

Step 1: Free Consultation

Step 2: Enrollment and Dedicated Account Setup

Step 3: Negotiation Phase

Profitable business ideas are often explored by people who want to take control of their money again. A creditor first agrees to a settlement. Then the offer is sent to you. You decide if you want to accept it or not. You are not forced at any point. If you agree, money from your dedicated account is used to pay it. The fee is usually 15–25% of your total debt. You only pay after a settlement is completed. There are no upfront charges.

Step 5: Program Completion

Mistakes People Make When Considering Debt Settlement

Building wealth takes careful decisions, and choosing the wrong debt relief service can make a tough situation even worse.

- Not understanding the credit score impact. Work from home options are often explored when people feel financial pressure. Debt settlement changes how you handle your payments. You must stop paying your creditors during the program. Because of this, your credit score usually drops. In most cases, this drop cannot be avoided. If you need strong credit in the next 2–4 years for a mortgage, car loan, or other loan, this is important to consider.

- Forgetting about the tax consequences. The IRS treats forgiven debt as taxable income. For example, if FFN settles $10,000 of your debt for $4,000, the $6,000 difference may count as income. The creditor can report this amount to the IRS using a 1099-C form. You must then include it on your tax return. Some exceptions exist, such as insolvency. You should always consult a tax professional before enrolling in any debt settlement program.

- Enrolling before exploring all options. Low investment business ideas attract people who want to improve their financial situation. Debt settlement is not always the best option. Some people may get better results from a nonprofit debt management plan through NFCC member agencies. Others may benefit from a balance transfer card or even bankruptcy. These options can sometimes have fewer downsides. You should review all alternatives carefully before making a decision.

- Expecting it to be a passive fix. Debt settlement with freedom financial network requires your active involvement. You must keep making regular deposits into your dedicated account. You also need to stay in contact with your debt consultant. When settlement offers come in, you must review them and make decisions. Treat the process like a serious financial project. It is not something that runs completely on its own.

What to Realistically Expect from Freedom Financial Network

Profitable business ideas attract people who want to rebuild their finances. The honest verdict on freedom financial network is that this company is legitimate and has a strong track record. It holds accreditation from the American Fair Credit Council (AFCC) and the International Association of Professional Debt Arbitrators (IAPDA). It is not a scam. However, debt settlement comes with real trade-offs. It can damage your credit, create tax implications, and require a multi-year commitment. You should think carefully before you choose this option.

Alternatives and Resources Worth Knowing

Before or after dealing with debt, here are resources I’d recommend:

- National Foundation for Credit Counseling (NFCC) , nfcc.org Free and low-cost nonprofit debt counseling. If your debt is manageable with a structured repayment plan, a nonprofit debt management plan may serve you better than settlement, with less credit damage.

- Consumer Financial Protection Bureau (CFPB) , consumerfinance.gov The US government’s consumer watchdog. Research any debt relief company here before signing anything. Check complaint history and verify licensing.

- Annualcreditreport.com (free) Pull your credit reports from all three bureaus, Equifax, Experian, and TransUnion, for free as part of using freedom financial network responsibly. Know exactly what’s on your report before entering any debt relief program.

Once you’ve resolved debt and are ready to start building income, check out ideas for passive income that actually work , that’s where the wealth-building phase begins.

If you want low investment business ideas to start generating extra income while managing debt, unique business ideas that actually work in real life is worth reading.

And if you’re looking for flexible income you can generate from home while your finances stabilize, online tutor jobs from home is a realistic starting point with low barriers.

The Bottom Line

Freedom Financial Network is a legitimate and established debt settlement company. It has helped hundreds of thousands of Americans reduce and resolve large unsecured debts. However, it is not the right choice for everyone. The program can lower your credit score. It may also create tax implications and requires a multi-year commitment. You should weigh these trade-offs carefully based on your personal financial situation.

If you have $7,500 or more in unsecured debt and feel like you are losing control each month, a free consultation can help. It costs nothing and gives you clear information to make a better decision. Knowledge is the first step toward improving your finances. Once you clear your debt, you can focus on building wealth and creating income streams. Native Money can guide you through this next stage. You can explore the site for practical and honest guides to grow your money, no matter where you start.

FAQ:

Freedom Financial Network

Is Freedom Financial Network legitimate?

How much does Freedom Financial Network charge?

Will Freedom Financial Network hurt my credit score?

Profitable business ideas attract people who want to recover financially while managing debt. A debt settlement program can lower your credit score. You must stop paying creditors during the process. Credit bureaus then record these missed payments. Most clients see a big drop in their credit score during the program. Credit recovery usually starts 12–24 months after the program ends. At that point, negative records start to age, and people begin building better credit habits again.