The confusion between these account types is very common. Most people know they should invest for retirement, but they don’t have a clear plan. They are not sure which account to use, when to use it, or why it matters. Once you understand what each account does, the answer becomes simple. But the financial industry often makes it confusing on purpose. This is especially true when people talk about 401k vs IRA vs Roth strategies for long-term investing.

This guide explains each account type in simple terms. It also shows how they are different from each other. You will learn the 401k 2026 limits, the contribution rules, and how much you can invest each year. In the end, you will know the best order to use these accounts for your retirement savings.

The Core Difference: Tax Now vs Tax Later

Roth accounts (Roth IRA and Roth 401(k)) work the opposite way. You contribute after-tax money, so there is no tax deduction today. But your money grows completely tax-free. In retirement, you can withdraw it with no taxes. If you expect the same or higher tax bracket later, Roth usually wins.

For most people under 40, Roth is often the better choice. They are usually in a lower tax bracket now than they will be later. Tax-free growth over many years becomes very powerful. These benefits matter even more as the 2026 401k contribution limit keeps rising, letting people save more for retirement.

401k vs IRA vs Roth IRA: Complete Breakdown for 2026

The 401k , Your First Priority if You Have an Employer Match

A 401k is an employer-sponsored retirement account. Contributions come out of your paycheck pre-tax (or after-tax for Roth 401k if your employer offers it), reducing your taxable income in the year you contribute. The 401k 2026 contribution limit is $23,500 for individuals under 50, and $31,000 for those 50 and older, including catch-up contributions. These limits are significantly higher than an IRA.

When comparing 401k vs IRA, the 401k’s biggest advantage is the employer match. Many employers match 50–100% of your contributions up to a percentage of your salary—this is an immediate, guaranteed return on your investment that almost nothing else can match. For example, if your employer matches 100% up to 4% of your salary and you earn $60,000 per year, that’s $2,400 in free money annually. Not contributing enough to capture the full employer match is one of the most costly mistakes in personal finance.

The Roth IRA , The Most Powerful Account for Most Americans Under 50

When evaluating 401k vs IRA, a Roth IRA is an individual retirement account that you open yourself, completely independent of your employer. The 2026 Roth IRA contribution limit is $7,000 for those under age 50 and $8,000 for those 50 and older. There are also income limits: the ability to contribute begins to phase out at $150,000 for single filers and $236,000 for married couples filing jointly in 2026. Above those thresholds, a Backdoor Roth IRA strategy may still be available, even for investors who are already maximizing their 2026 401k contribution limit.

Why Is the Roth IRA So Powerful in the 401k vs IRA vs Roth IRA

Debate?

Three reasons. First, with complete investment flexibility, you can invest in anything available at your brokerage rather than being limited to your employer’s fund menu. Second, there are no required minimum distributions (RMDs), unlike traditional IRAs or 401(k)s. Third, Roth IRA contributions can be withdrawn anytime without penalty, adding flexibility. Even investors focused on the 401k vs ira vs roth decision often prioritize the Roth IRA after securing their employer match.

Open a Roth IRA at Fidelity or Vanguard , both offer zero-fee index funds and no account minimums. This is where I’d put money after capturing any employer 401k match.

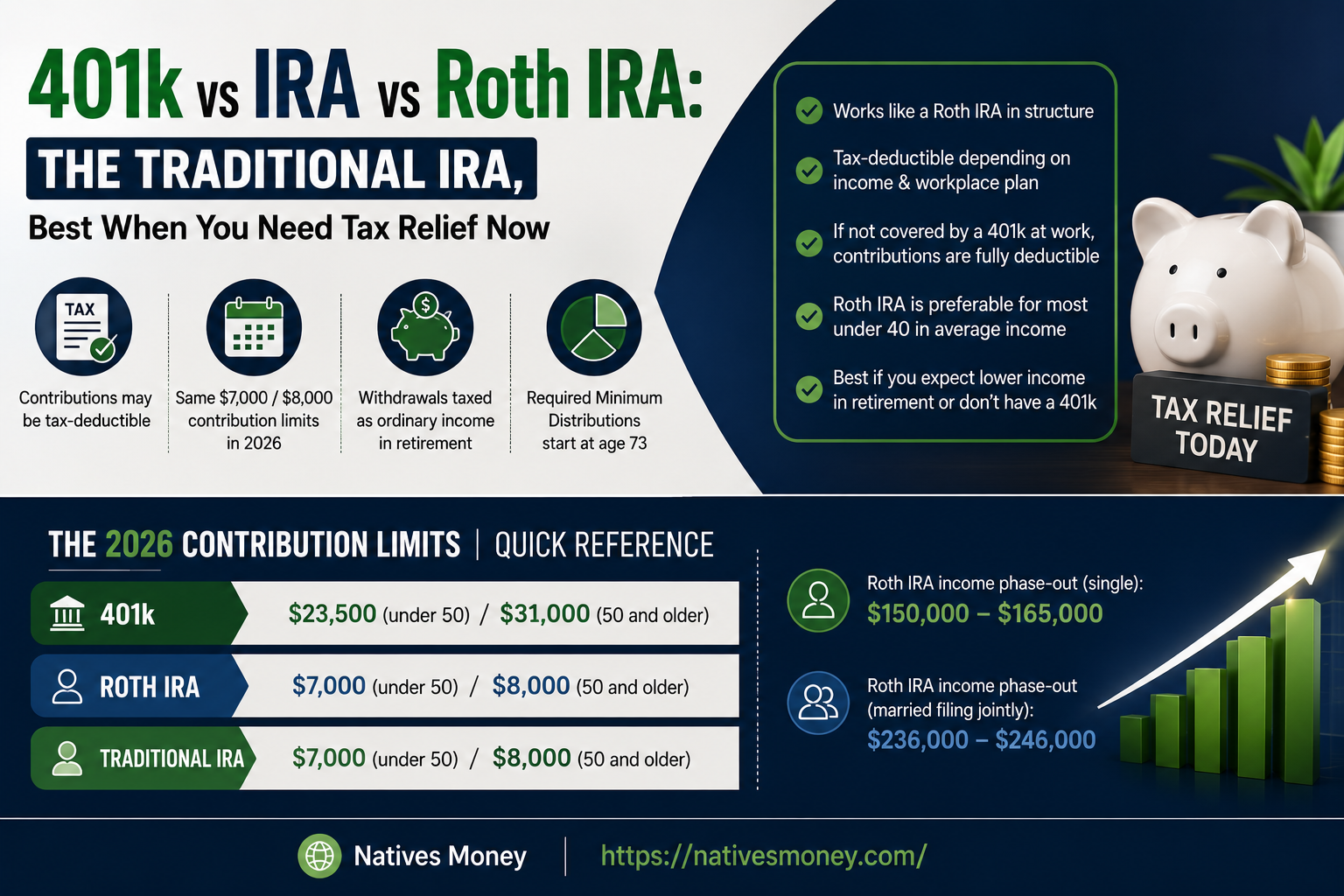

401k vs IRA vs Roth IRA: The Traditional IRA , Best When You Need Tax Relief Now

A traditional IRA works similarly to a Roth IRA in structure , you open it yourself, same $7,000/$8,000 contribution limits in 2026 , but contributions may be tax-deductible depending on your income and whether you or your spouse have a workplace retirement plan. If you’re not covered by a 401k at work, traditional IRA contributions are fully deductible regardless of income.

Withdrawals in retirement are taxed as ordinary income, and you must start taking required minimum distributions at age 73. For most people under 40 in average income brackets, a Roth IRA is often preferable. However, when comparing 401k vs IRA, if you’re in a high-income year and expect lower income in retirement, the traditional IRA’s tax deduction today may be more valuable. This can make a traditional IRA a smart choice depending on your current and future tax situation.

The 2026 Contribution Limits , Quick Reference

Here are the key numbers for 2026 at a glance:

- 401k 2026 contribution limit: $23,500 (under 50) / $31,000 (50 and older)

- Roth IRA 2026 contribution limit: $7,000 (under 50) / $8,000 (50 and older)

- Traditional IRA 2026 contribution limit: $7,000 (under 50) / $8,000 (50 and older)

- Roth IRA income phase-out (single): $150,000 – $165,000

- Roth IRA income phase-out (married filing jointly): $236,000 – $246,000

401k vs IRA vs Roth IRA: The Recommended Priority Order for Retirement Investing

Here’s the order I’d follow , and the order most financial planners recommend for the majority of Americans:

- Contribute to your 401k up to the full employer match (free money , never leave this on the table)

- Max out your Roth IRA ($7,000 in 2026) for tax-free growth and maximum flexibility

- Go back and increase 401k contributions toward the full $23,500 limit

- Any additional savings go into a taxable brokerage account

Common Mistakes People Make With These Accounts

These mistakes are all completely avoidable with the right information upfront.

- Not contributing enough to get the full 401k employer match. When discussing 401k vs IRA, one of the biggest mistakes you can make is missing out on your employer match. I made this mistake myself a few years ago. If your employer matches 3% of your salary, contribute at least 3% to your 401k. Failing to do so means turning down free compensation. There is virtually no financial reason to leave an employer match uncaptured, since it provides an immediate return on your contribution.

- Choosing a traditional IRA when a Roth IRA is better. When comparing 401k vs IRA, most people under 40 earning less than $100,000 per year may benefit more from a Roth IRA than a traditional IRA. The potential for decades of tax-free growth often outweighs the value of an immediate tax deduction today. This is especially true if future tax rates end up being higher, which many economists believe is possible. Over the long term, tax-free withdrawals can make a significant difference in retirement wealth.

- Investing 401k contributions in high-fee funds. Most 401k plans include a mix of low-cost index funds and expensive actively managed funds. Always look at the expense ratio of every fund option in your plan. Choose the lowest-cost index funds available , even if they’re not labeled prominently. A 1% expense ratio versus 0.05% can cost you $100,000+ over a 30-year career.

- Cashing out a 401k when changing jobs. One important consideration in 401k vs IRA planning is what happens when you leave an employer. You’ll typically receive paperwork asking what to do with your 401k balance. Cashing it out can trigger income taxes and a 10% early withdrawal penalty if you’re under age 59½. In most cases, rolling the funds into an IRA is the better option because it preserves your tax advantages and keeps your investments growing. The rollover process is usually straightforward and can help protect years of compound growth.

What These Accounts Can Realistically Do for You Over Time

The math behind consistent investing in the 401k vs ira vs roth ira strategy is genuinely remarkable, not because returns are spectacular every year, but because compounding becomes incredibly powerful over decades inside tax-advantaged accounts.

A 25-year-old who maxes out a Roth IRA ($7,000/year) invested in a total market index fund averaging 8% annually has approximately $2.1 million by age 65 , completely tax-free. If they also captured a 3% employer 401k match on a $55,000 salary ($1,650/year) every year, add another $440,000 to that figure. All from consistent, boring, automated contributions started at 25.

What the 401k vs ira vs roth ira Comparison Really Comes Down to in Practice

use all of them in the priority order above, contribute consistently, and invest in low-cost index funds within each account. The account type optimization matters, but showing up consistently matters far more. Even someone who chose the wrong account type but contributed faithfully for 30 years ends up significantly wealthier than someone who optimized the account type but contributed irregularly, even when trying to maximize the 401k 2026 contribution limit.

Best Platforms to Open These Accounts in 2026: 401k vs IRA vs Roth IRA

Here’s where I’d actually open each account today:

- Fidelity (free, zero minimums) , My top recommendation for both Roth IRAs and IRA rollovers. Zero expense ratio index funds (FZROX, FZILX), no account minimums, excellent interface, and one of the best mobile apps in the industry. Open a Roth IRA in 15 minutes online.

- Vanguard (free) , When researching 401k vs IRA investment options, Vanguard is often one of the most respected platforms for long-term investors. It pioneered index fund investing and is known for its low-cost funds. While some Vanguard mutual funds have higher minimum investment requirements than Fidelity, its popular ETFs—such as VTI, VXUS, and BND—have no minimum investment. Vanguard’s unique investor-owned structure also means profits are returned to fund shareholders rather than outside corporate owners.

- IRS.gov Retirement Plans page (free) , When researching 401k vs IRA rules, it’s important to verify current contribution limits, income thresholds, and eligibility requirements using official IRS information. These figures are updated regularly, and the IRS remains the most reliable source for accurate, up-to-date guidance. While third-party articles can be helpful, official IRS resources should always be your final reference when making retirement planning decisions.

Once you’ve got your retirement accounts set up and funded, the natural next step is understanding how to invest the money inside them. For how growth stocks fit into a long-term account strategy, growth stocks: how to identify high-growth companies for long-term investment success is worth reading.

For value-oriented investing inside your retirement accounts, value stocks: the smart investor’s guide to finding undervalued market opportunities gives you the framework.

And for a complete set of investment strategies to use within these accounts, investment strategies: 15 smart ways to build long-term wealth in 2026 covers every approach worth knowing.

The Bottom Line

The 401k vs IRA vs Roth IRA decision comes down to one practical framework: capture your employer’s 401k match first (free money), then max a Roth IRA for tax-free growth and flexibility, then increase 401k contributions toward the annual limit. For most Americans under 40 in moderate tax brackets, the Roth IRA is the single most powerful account available , and yet most people either don’t have one or haven’t maximized it.

Open a Roth IRA at Fidelity today if you don’t have one. It takes 15 minutes and the compounding starts the moment your first contribution is invested. The best time to start was when you got your first paycheck. The second best time is right now in the 401k vs ira vs roth planning framework. Keep exploring Native Money for honest, practical guides on building wealth at every stage of your financial journey.

FAQ:401k vs IRA vs Roth IRA in 2026

What is the difference between an IRA, Roth IRA, and 401k?

In the 401k vs ira vs Roth framework, a 401k is employer-sponsored with higher contribution limits ($23,500 in 2026) and potential employer matching. A Traditional IRA is individually opened with pre-tax contributions (tax deduction now, taxes in retirement) and a $7,000 limit in 2026. A Roth IRA is individually opened with after-tax contributions (no deduction now, but all growth and withdrawals are tax-free in retirement) with the same $7,000 limit. The priority order for most Americans: 401k to employer match, then Roth IRA, then more 401k.

What is the 401k contribution limit for 2026?

Understanding contribution limits is an important part of 401k vs IRA planning. The 2026 401(k) contribution limit is $23,500 for employees under age 50 and $31,000 for those age 50 and older, thanks to the additional $7,500 catch-up contribution. These limits apply to your combined traditional and Roth 401(k) contributions. Employer matching contributions do not count toward the employee limit. The total annual limit, including both employee and employer contributions, is $70,000 in 2026.

Should I choose a 401k or Roth IRA first?

The correct order for most Americans is simple. First, contribute to your 401(k) up to the full employer match. Next, max out your Roth IRA ($7,000 in 2026). After that, go back to your 401(k) and increase contributions toward the $23,500 limit. This plan in the 401k vs IRA vs Roth IRA strategy helps you get free employer money first. It also helps you grow money tax-free and use higher retirement limits in the best way.

What are the 2026 401k limits for people over 50?

When comparing 401k vs IRA, it’s important to understand contribution limits. The 2026 401(k) contribution limit for people age 50 and older is $31,000, which includes the standard $23,500 employee contribution limit plus a $7,500 catch-up contribution. There is also a special provision for workers ages 60 to 63 under the SECURE 2.0 Act that allows a higher catch-up amount. Check the IRS each year for the latest figures, as limits can change. Maximizing these contributions during your final working years can significantly strengthen your retirement savings.

Yes, absolutely. You can have both a 401(k) from your job and a Roth IRA you open yourself. This is not only allowed, it is also the best plan for most people in the 401k vs IRA vs Roth IRA system.

These are different accounts. Each one has its own rules and limits. If you put money into your 401(k) up to the 2026 401k contribution limit ($23,500), it does not stop you from adding $7,000 to a Roth IRA in 2026.

There is one limit to know. The Roth IRA has an income rule. If your income is above about $165,000 as a single filer, you may not be able to contribute directly to a Roth IRA. But you can still use a Backdoor Roth IRA. This lets high earners still get tax-free growth.